by Andrea Gnetti, CEO of Excellence Payments

Creating new offerings in a regulated market such as payments is a complex process. Product designers often encounter objective technical obstacles that limit development possibilities. This requires us to often make compromises, modifying the original design. The development of the Digital Euro is in this state. This is what emerges from the latest report from the ECB (European Central Bank) on the development of the Digital Euro, published on 25 June 2024.

The investigation phase, which ended at the beginning of October 2023, presented an ambitious plan to the market; a new payment circuit that promises to do things not possible with existing solutions on the market today, with a strong focus on creating simple and fluid user experiences. The technical investigations carried out in recent months have highlighted how the promises made are not easy to keep.

The risk is that we fall into the temptation to make things happen at any cost. It is understandable that the ECB’s task of collaborating with all interested parties, starting with the banks, and then finding a point of agreement with Parliament and the European Commission, is not at all easy. This situation could push towards the acceptance of excessive compromises. However, the launch of a Digital Euro with too many restrictions and, even worse, with an inadequate level of service, would inevitably compromise its development. This would generate distrust in payment service providers, who would not be willing to seriously invest in building ecosystems based on it.

The symptoms of this “disease” emerge from two analyzes conducted by the ECB for the benefit of the Commission and the European Parliament. These aim to direct some development choices for the functions of the Digital Euro following an analysis of the possible implementation options:

- Provide multiple Digital Euro wallets to a single user

- Allow anonymous offline transactions in person

Provide multiple Digital Euro wallets to a single user

The Digital Euro will be distributed by payment service providers, be they banks, EMIs or payment institutions. For the initiative to be successful, the European payments system must see it as a business opportunity. Limiting wallet ownership to one per user, a solution preferred by the ECB[1], could restrict the market from the start.

The regulator’s intent is to create a free basic platform for consumers, where service providers can add value-added solutions, even for a fee, to build profitable business propositions. Whoever manages to provide their customer with a Digital Euro wallet, if they can only have one, will have an advantageous position over all competitors, being the only one able to access current accounts at zero costs and in real time of the customer even on different banking operators.

This operator would have every interest in creating barriers to the customer’s exit, holding the possibility of offering services that are precluded to others. Those operators who wanted to propose an alternative to that customer would have to convince him to abandon the current services for their own, without even having been able to try them in their full functionality.

The risk is that in this way the offers of a few large generalist operators will be favored, capable of concentrating sufficient investments in the initiative with the prospect of a return in the medium-long term. This is on the assumption that the process of adopting the new payment instrument will be slow. We have already found in the past that changing payment habits, even by switching to better tools, takes time. An example of this is the slowness with which smartphone payments are establishing themselves over contactless card payments, despite guaranteeing a simpler experience of use for all amounts.

A single wallet per customer would therefore limit the market to a few large operators, inhibiting the creation of new innovative offers in niche sectors, typical of the fintech world.

The reason indicated by the ECB for preferring this option lies in the complexity that managing multiple digital wallets would have in the presence of a maximum threshold of possession of Digital Euros per user. This threshold, yet to be defined, was created to prevent Digital Euro wallets from being used as savings tools, with the risk of draining an important source of business for banks. In practice, in addition to the technical difficulties, it would be complex for a user to manage the availability of Digital Euros in a context of multiple digital wallets.

Without having participated in the ECB’s analysis, we cannot claim here to indicate what the best approach is. We simply observe that the compromise proposed to simplify the technological solution is excessive and could hinder its success from the beginning. We believe that it is necessary to make an effort to explore new solutions, even different from those currently proposed, in order to ensure that every European citizen can have multiple Digital Euro wallets at the time of launch. This decision could also justify a possible postponement of the launch times.

Allow anonymous offline transactions in person

The possibility of carrying out anonymous transactions between two individuals in Digital Euros, of a limited amount (threshold to be defined) and in person, is one of the most original aspects of the Digital Euro. The decision to implement this functionality arises from the need expressed by European citizens, who indicate the anonymity of transactions as the first reason for using cash, on a par with expense control[2].

Another advantage, of less importance than the first, is the possibility of paying in Digital Euro even in non-connected areas.

The ECB[3] has conducted a preliminary analysis which highlights the need to use the Secure Element in our smartphones to ensure secure and easy-to-use functionality. The Secure Element is the component that protects our transactions when we use digital wallets, such as Apple Pay and Google Wallet.

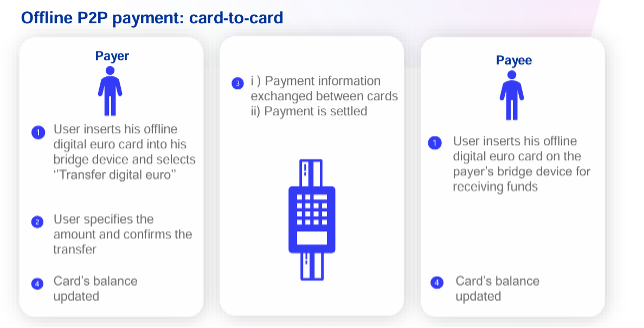

Despite the efforts of European regulators to extend the use of this component to third parties, the commitments made by smartphone manufacturers, in particular Apple[4], do not yet fully guarantee this possibility. Furthermore, adapting to the different solutions implemented by manufacturers makes the implementation of the service complex. These considerations have pushed the ECB to explore a possible alternative solution based on the use of a bridging device, into which cards can be inserted to carry out transactions. However, considering that the Digital Euro is designed to be managed mainly via digital wallet and not via a physical card, which should only be provided in exceptional cases to promote financial inclusion, and which would oblige users who intend to carry out this type of transactions to always have an external device, we believe that this solution is not suitable for this purpose.

In this case it is necessary to persevere in the search for a solution that contemplates the exclusive use of smartphones, possibly postponing the launch of this functionality to a second phase, aware of the fact that the Digital Euro will complement and not replace cash, which therefore it can still be used as an alternative.

[1] Fonte: BCE – Technical note on the provision of multiple digital euro accounts to individual end users – 25 Marzo 2024

[2] Fonte: BCE – Study on the payment attitudes of consumers in the euro area (SPACE) – 2022

[3] Fonte: BCE – State of play on offline Digital Euro – 11 Aprile 2024

[4] Fonte: BCE – Feedback on commitments offered by Apple over access restrictions to near-field communication technology – 19 Aprile 2024